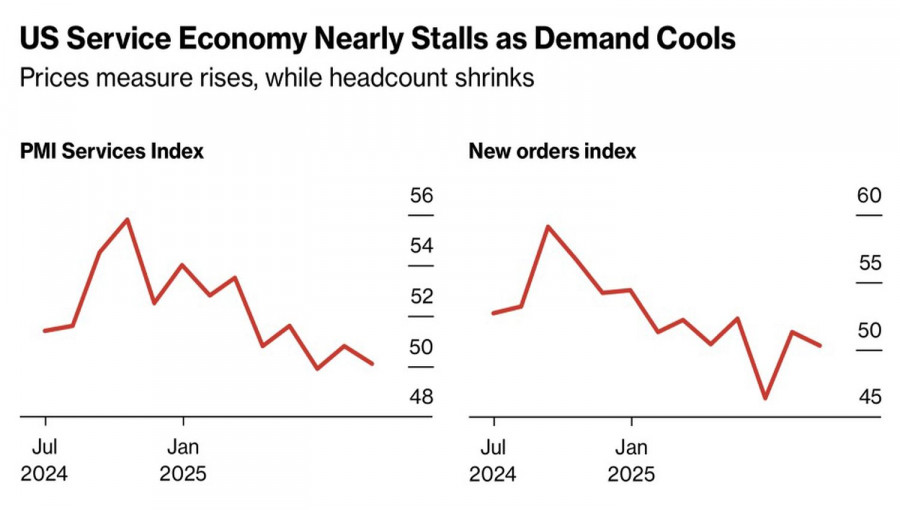

The specter of stagflation is once again haunting financial markets. The ISM services employment index has declined for the fifth time in the past six months, while the price index surged to its highest level since 2022. Business activity in the U.S. services sector points to stagnation in the economy, and investors are finally starting to take notice. They may regret having bought the dip in the S&P 500.

Before the July U.S. jobs report, stock indices had shrugged off both Donald Trump's tariff threats and the Federal Reserve's reluctance to cut rates. The U.S. economy appeared to rest on a solid foundation—enough to support new record highs in the S&P 500. But a cooling labor market has changed the picture.

The broad stock index is reacting nervously to White House threats to raise import duties on India due to its purchases of Russian oil, including plans for tariffs on pharmaceuticals, potentially increasing them to 250%.

Even growing investor confidence in Fed rate cuts is failing to provide support. Futures markets now assign a 48% chance of three rate cuts in 2025—essentially one at each remaining FOMC meeting this year. Interestingly, Jefferies research shows that since 1990, the equal-weighted S&P 500 has outperformed the traditional index during Fed easing cycles. This suggests that the former rally leaders—the so-called "Magnificent Seven"—could soon be outpaced by small-cap stocks.

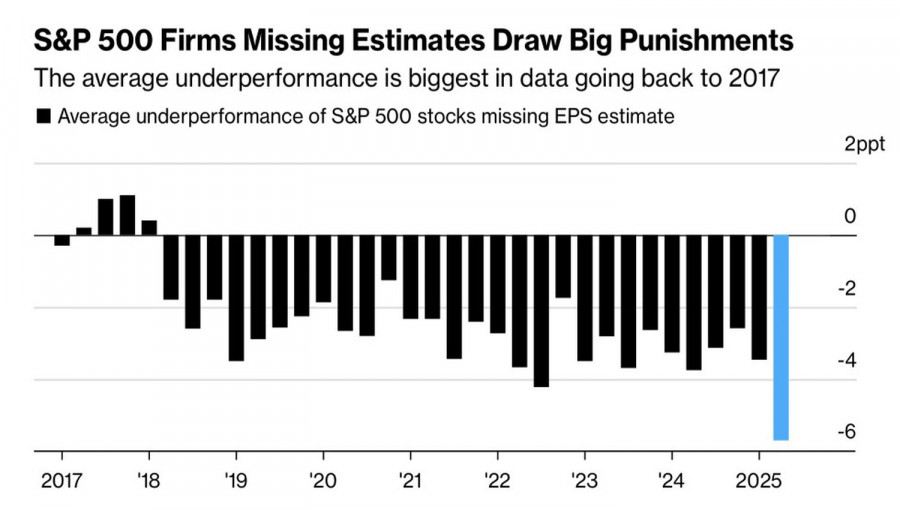

Investors are also showing fatigue with earnings season, typically seen as a bullish factor. On the one hand, second-quarter results have beaten Wall Street consensus estimates by 9.1%, the highest margin since 2021. However, the bar was already low, and companies that fall short of expectations are being hit with record sell-offs.

Trump's attacks on the Fed chair and the dismissal of the head of the Bureau of Labor Statistics over allegedly falsified U.S. employment data are making markets jittery. The concern is that new leaders at the Fed and BLS will simply follow the president's directives. Statistics will become politically convenient, and the Fed—despite supposedly strong economic data—will still move to cut rates. This would make the U.S. resemble Turkey, where Recep Tayyip Erdogan's interference in the central bank led to a massive currency crisis.

Who Would Want U.S. Assets in That Case? Capital outflows from the U.S. to Europe and other regions could trigger broad sell-offs in the S&P 500.

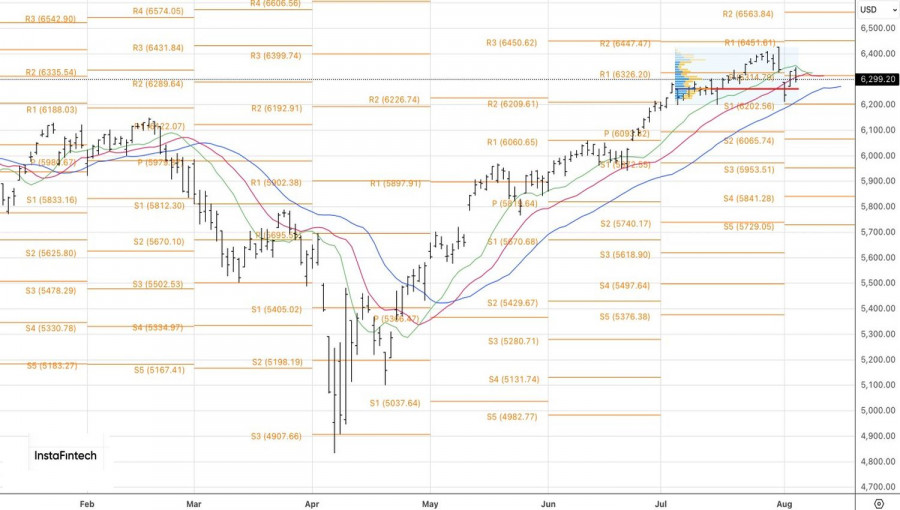

Technically, the daily S&P 500 chart shows a successful break below the pivot support level at 6315, which opened the door for short positions. A drop below 6285 and the fair value area of 6260 would justify adding to those shorts.